{kind=link}

Loan Agreement with Guarantor

Our Loan Agreement with Guarantor template:

- Includes guarantor provisions

- UK Solicitor-drafted for reliability

- Clear, plain English

- Full satisfaction guarantee

How Does It Work?

-

1. Download

-

2. Edit

-

3. Print

-

4. Sign

This Loan Agreement With Guarantor template is a variation of our standard loan agreement template.

How does the guarantee provision work?

Our draft comes with the clauses to enable you to require a further person (or company) to stand as guarantor for the loan. The guarantor will guarantee the performance of the contract, in the sense that they will be responsible to see that either:

- the original borrower repays the loan and interest, or

- the guarantor will have to do so instead.

For this to be of real use, the guarantor needs to be a person with good financial wherewithal (even more so than the borrower).

Using our Guaranteed Loan Agreement template

The template has been drafted so that it can be edited to provide for the loan to be:

- interest-bearing, or

- interest-free.

You can amend the template so that the loan is for:

- a fixed period, or

- repayable by instalments, or

- repayable on demand.

The loan agreement can be between companies or individuals.

It is downloadable in Word format. It includes full guidance notes, which make it exceptionally easy to complete. You then just need to print it and have all the parties sign the document.

Guide to our Guaranteed Loan Agreement

Our Loan Agreement With Guarantor template is for use by someone who has made a loan or who is wishing to make a loan, but wants the repayment guaranteed by someone else.

This loan agreement incorporates various options, so it is appropriate whether:

-

interest is being charged or not;

-

the loan is repayable in full in one lump sum or over a period by instalments; and

-

the lender and borrower are companies or individuals.

This template presumes that:

-

there is a guarantor of the loan; but

-

no other security is being provided to the lender for the loan.

If these are not the case, then you may need one of Legalo’s other loan agreement templates that would better suit you.

Clauses in this Guaranteed Loan Agreement

Below, we note the clauses that differ from the basic loan agreement. You can preview the guide to the rest by looking at the guide to the basic loan agreement – click here.

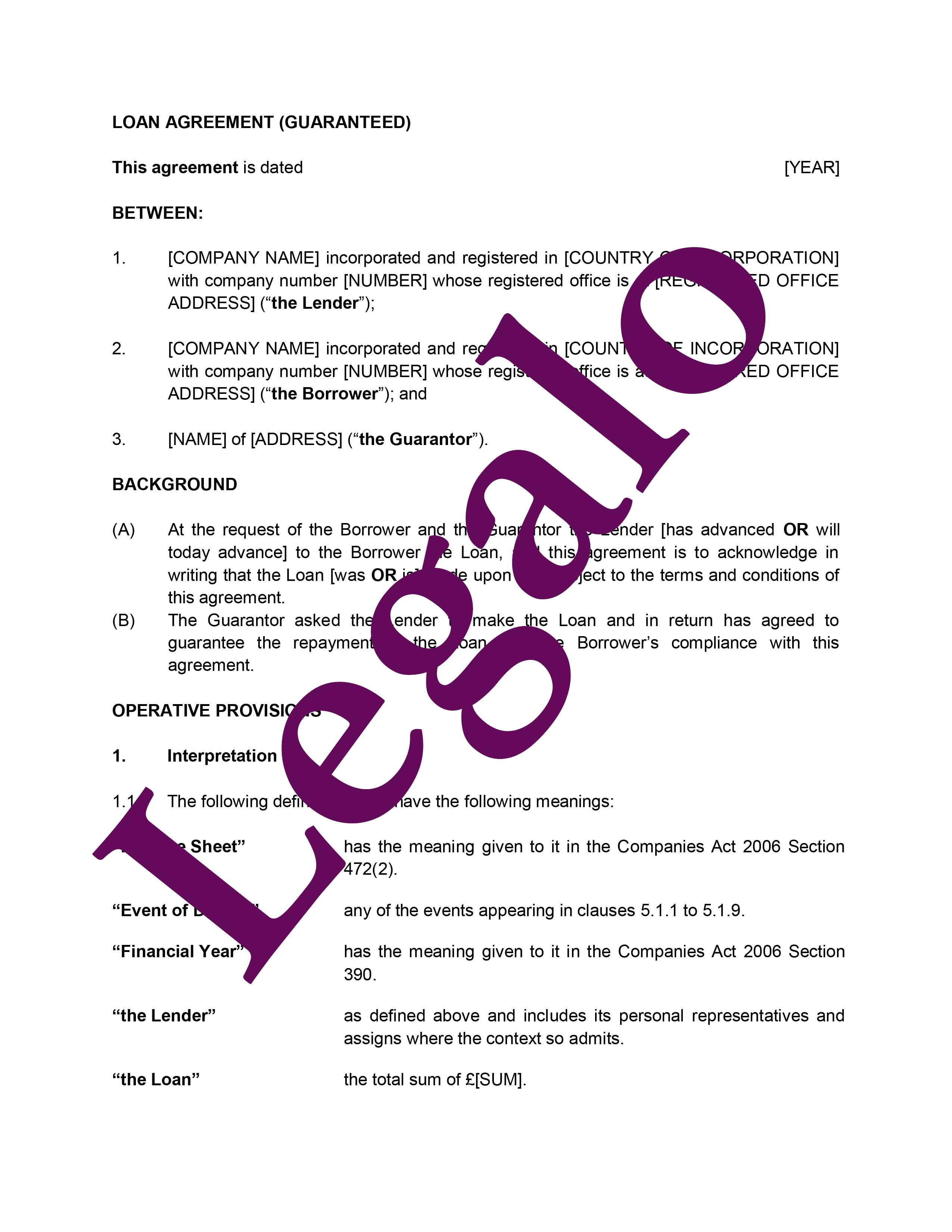

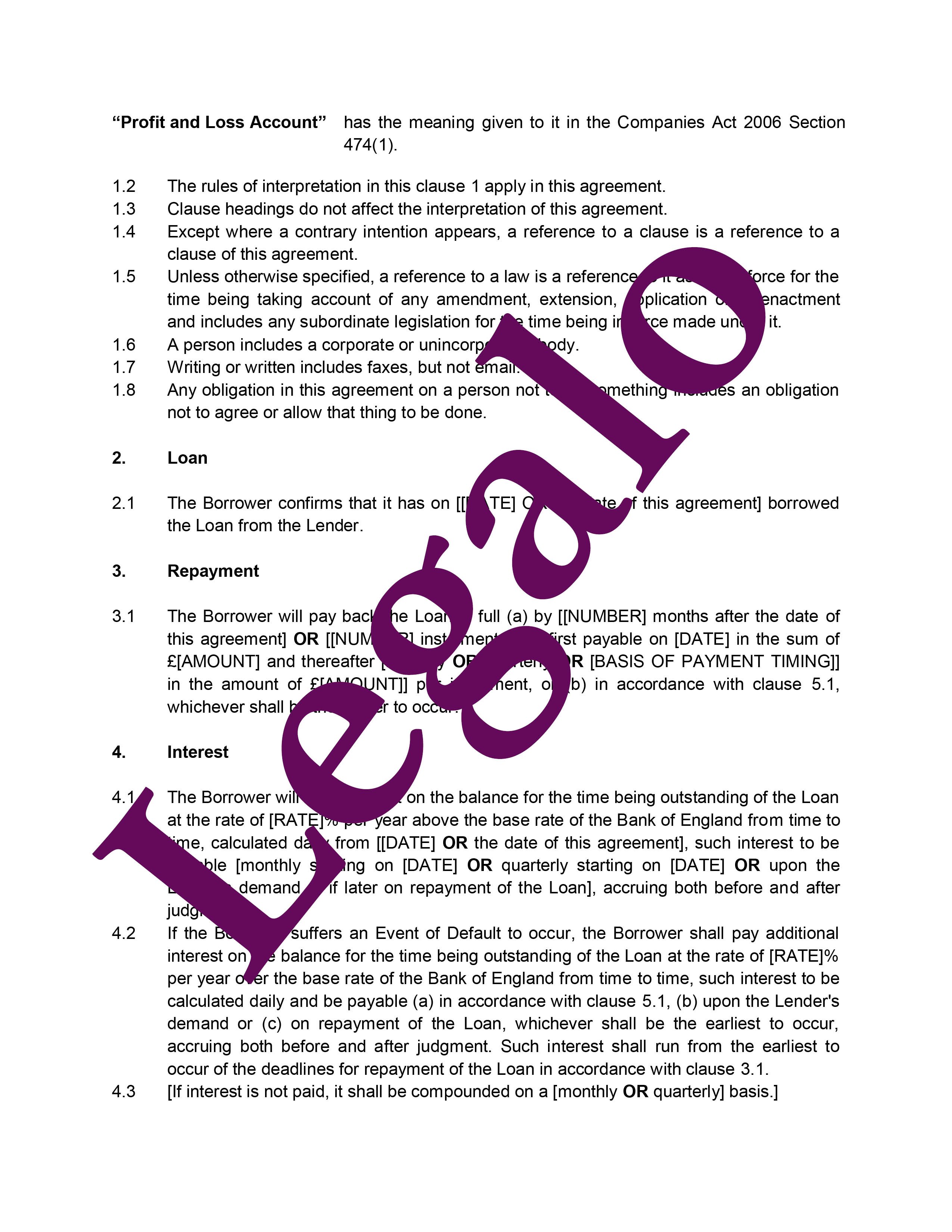

7. Guarantor – This is the clause under which the guarantor gives the lender a guarantee that the borrower will comply with the terms of the agreement and repay the loan. Note that no guarantee is valid if only verbal – it must be in writing for you to be able to rely on it (section 4 of The Statute of Frauds 1677).

12. Counterparts – As the agreement is being signed as a deed, this clause provides that you can have sufficient prints of it signed by each party separately and held by the other parties if you wish (i.e. they don’t all have to sign the same physical print).

It also explains how to sign the document as a deed validly.

For more about guarantees, have a look at Wikipedia.

FAQs on a Guaranteed Loan Agreement

Below, we address the top questions on this topic from the Internet.

Can you draw up your own loan agreement?

Yes, you can draw up your own loan agreement. To ensure that your agreement includes all essential terms and follows the law, while avoiding spending a large sum on solicitors, you can use our great Legalo template. It will make the process quick and simple for you.

How do I write a legal loan agreement UK?

To write a legal loan agreement in the UK, include the following key elements:

- Parties involved: Identify the lender and borrower, including their full names and addresses.

- Loan amount and terms: Clearly state the loan amount, interest rate (if any), repayment schedule, and due dates.

- Guarantor (if applicable): Include details of the guarantor and their obligations.

- Collateral (if any): Specify any assets used as collateral for the loan, along with their details.

- Signatures and date: Ensure all parties sign and date the agreement to make it legally binding.

How do I write a loan agreement between friends?

A loan agreement between friends should include all of the key components of any loan agreement, such as details of the parties involved and of the loan itself, repayment terms, details of interest due, security to be provided, signatures and dates, and any other relevant information. It is advised to keep it simple and clear to avoid misunderstandings and disputes among people with an existing relationship, such as friends or family.

How do I write a private loan agreement?

A private loan agreement should include all of the key components of any loan agreement, such as:

- details of the parties involved;

- details of the loan;

- repayment terms;

- interest charged;

- any security being provided by the borrower; and

- any other relevant information.

What makes a valid loan agreement?

As long as your contract includes all of the key components of a loan agreement, such as details of the parties involved and of the loan itself, terms and conditions, signatures and dates, it will be valid. This means that your agreement is legally binding. If you use our draft, you can be safe in the knowledge that your document will be enforceable.

For a loan agreement that is guaranteed, it must be in writing in order to be enforceable and binding on the guarantor. This is because of the Statute of Frauds 1677, which states that a verbal guarantee is not valid.

Does a loan agreement need to be witnessed in the UK?

In the UK, it is not a strict requirement to have a loan agreement witnessed for it to be valid. However, if you have a guarantor for the loan, then the parties should sign the loan agreement as a deed, i.e. with a witness, so that it is binding on the guarantor, who may not otherwise be receiving any value from the contract. Our template is drafted in this manner.

Can you still get a loan with a guarantor?

Yes, you can still get a loan with a guarantor. A guaranteed loan involves a third party, typically with a strong credit history, who agrees to repay the loan if the borrower defaults. This arrangement can help individuals with weaker credit profiles or limited financial history qualify for loans. However, it’s important to find a willing and eligible guarantor, and all parties should fully understand their responsibilities before proceeding with such a loan.

What is the guarantor clause in a loan agreement?

A guarantor clause in a loan agreement is a provision where a third party guarantor agrees to assume responsibility for repaying the loan in the case the primary borrower defaults on their duties. The clause must clarify the guarantor’s obligations and specify any scenarios in which these responsibilities may come into play.

What does a guarantor need to provide for a loan?

A potential guarantor typically needs to provide proof of their financial stability, such as proof of income, credit history, and personal identification. Guarantors should have a good credit score and be aware of the potential financial risks that this involves, in case the borrower fails to repay the loan. Lenders will also require the guarantor to sign a legally-binding agreement, acknowledging their responsibility for repaying the loan if the borrower defaults.

What are the rules for loan guarantors?

A set of criteria must be met for an individual to be a valid guarantor for a loan:

- Creditworthiness: A guarantor should have a good credit rating to ensure they will be able to take on any financial responsibilities as a result of a defaulted loan.

- Informed Consent: Guarantor’s should fully understand their obligations and consent willingly.

- Legal age: A guarantor must be of legal age to be able to enter into binding legal contracts.

- No coercion: If a guarantor is seen to be under duress when agreeing to their new obligations, this can jeopardise the agreement, as they may not have willingly given their consent. For this reason, some lenders will require the guarantor to take independent legal advice. You would then ask your legal adviser to complete a independent legal advice certificate for the lender. (Use our template for that if the lender does not have their own preferred form.)

While it is not a legal requirement under English law, in practical terms, it is best if the guarantor is completely clear on what they are agreeing to.

What are the disadvantages of a guarantor loan?

The main risk that comes with a guarantor loan is that the guarantor can become fully liable for the repayment of the loan and interest as well as enforcement costs if the borrower defaults, thus risking their own credit and finances. From this can come a strained relationship between borrower and guarantor in the future, meaning that the fallout may not be solely financial. It can also be difficult to find a willing and eligible guarantor. This is because the role comes with a lot of responsibility and very important criteria that an individual must meet.

Can a guarantor be forced to pay?

Yes, the lender can legally oblige a guarantor to pay if the borrower fails to, as that:

- is the purpose of a guarantor’s role in a loan agreement; and

- is what the guarantor has agreed to when they signed the document.

When the borrower fails to make payments as agreed, the lender can pursue the guarantor for repayment, in accordance with the terms set out in the agreement.